2022-2027 Market Forecast

Pressed & Blown Glass & Glassware Manufacturing| Market Forecast | Full Report | |

|---|---|---|

| Current State of the Industry |  |

|

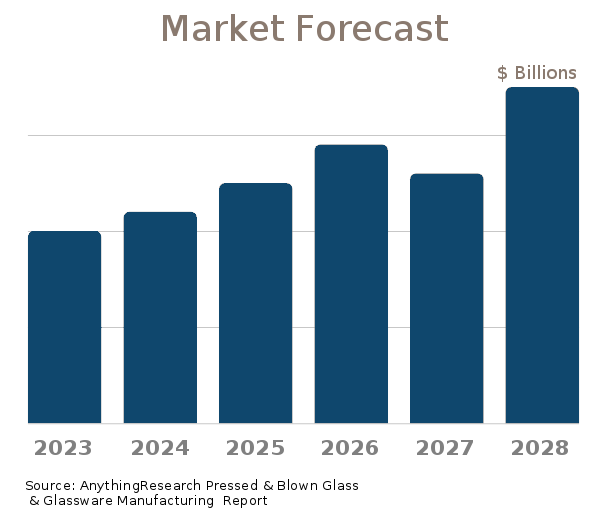

| Market Forecast (2022-2027) | |

|

| Market Size (2017-2021) | |

|

| Market Landscape - Leading & Disruptive Companies | |

|

| Innovation News | |

|

| Products/Services Breakdown | |

|

| Market Size - per State | |

|

| Financial Metrics | |

|

| Salary & Compensation Statistics | |

|

| Key Companies | |

|

| Government Vendors | |

|

| Instant Download - Available immediately upon purchase | |

|

| Download now: |

2022-2027 Pressed & Blown Glass & Glassware Manufacturing Market Forecast

U.S. Market Forecast & Outlook

Forecasting the trends in the market size for the Pressed & Blown Glass & Glassware Manufacturing industry is a necessary part of the business planning process. AnythingResearch forecasts are used by- Financial institutions seeking to understand credit-worthiness prior to lending

- Investors evaluating startups, venture opportunities, and equities

- Corporations setting strategy and sales & marketing objectives

- Startups demonstrating the "market opportunity" for their business

| Forecast / Industry Outlook | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 |

|---|---|---|---|---|---|---|

| Market Forecast ($ millions) | ||||||

| Projected Industry Growth Rate (%) | ||||||

The future growth of the Pressed & Blown Glass & Glassware Manufacturing is influenced by internal and external factors. Internal factors include structure and competition within the industry, market demand, and innovative and disruptive factors. External factors include the state of the economy and cyclical patterns.

Pressed & Blown Glass & Glassware Manufacturing Competitor Landscape & Key Companies [PREMIUM]

The most influential companies in the Pressed & Blown Glass & Glassware Manufacturing industry and adjacent industries either have large market share or are developing new business models and methods that could disrupt the status quo. We look at leading and emerging companies in the Pressed & Blown Glass & Glassware Manufacturing industry and adjacent sectors:| Market Leaders: Direct Competitors Companies with the largest market share, focused in this industry |

Market leaders: Diversified Competitors Largest companies that have diversified operations in this and other industries |

| Innovators: Direct Competitors Innovative, Emerging, and Disruptive Companies that may influence the future direction of the industry. |

Innovators: Diversified Competitors Innovators and Disruptors in adjacent industries that may also affect the Pressed & Blown Glass & Glassware Manufacturing industry. |

Source:

Innovation News

Executive Briefings

We compete with many large and varied manufacturers, both domestic and foreign. Some of these competitors are larger than we are, and some have broader product lines. We strive to maintain and improve our market position through technology and product innovation. For the foreseeable future, our competitive advantage lies in our commitment to research and development, deep customer relationships, reliability of supply, product quality, superior customer service and technical specification of our products. There is no assurance that we will be able to maintain or improve our market position or competitive advantage.  Optical Communications Segment  We maintain a leadership position in the segmentâs principal product groups, which include carrier and enterprise networks. The competitive landscape includes industry consolidation, pricing pressure and competition for the innovation of new products. These competitive conditions are likely to persist. Our large-scale manufacturing experience, fiber process, technology leadership and intellectual property provide cost advantages relative to several of our competitors. Our principal competitors include CommScope Holding Company, Inc. and Prysmian Group S.p.A.  Display Technologies Segment  We are the largest worldwide producer of glass substrates for flat panel displays. The environment for high-performance display glass substrate products is very competitive and we have maintained our competitive advantages by investing in new products, continually improving our proprietary fusion manufacturing process and providing a consistent and reliable supply of high-quality products. Our process allows us to deliver glass that is larger, thinner and lighter, with exceptional surface quality and without heavy metals. Our principal competitors include AGC Inc. and Nippon Electric Glass Co., Ltd.  Specialty Materials Segment  We have deep capabilities in materials science, optical design, shaping, coating, finishing, metrology and optical system assembly. Our products and capabilities in this segment position us to meet the needs of a broad array of markets, including semiconductor, aerospace, defense, industrial, commercial and telecommunications. Our principal competitors include Schott AG, AGC Inc., Nippon Electric Glass Co., Ltd.  Environmental Technologies Segment  We maintain a strong position in the worldwide market for automotive ceramic substrate and filter products, as well as in the heavy-duty and light-duty diesel vehicle markets. Our competitive advantage in automotive ceramic substrate products for catalytic converters and filter products for particulate emissions in exhaust systems is based on an advantaged product portfolio, collaborative engineering design services, customer service and support, strategic global presence and continued product innovation. Our principal competitors include NGK Insulators, Ltd.  Life Sciences Segment  We seek to maintain a competitive advantage by emphasizing product quality, global distribution, supply chain efficiency, a broad product line, technical support and superior product attributes. Our principal competitors include Thermo Fisher Scientific Inc., Avantor, Inc., Greiner AG, Eppendorf SE, Sarstedt AG Corning

Related Reports

Can't find what you're looking for? We have over a thousand

market research reports.

Ask us and an analyst will help you find what you need.