| Standard Report | Premium Report | |

|---|---|---|

| Current State of the Industry |  |

|

| Market Size (industry trends) | |

|

| Market Forecast (5-year projection) | |

|

| Products/Services Breakdown | |

|

| Revenue per State | |

|

| Financial Metrics | |

|

| Salary & Compensation Statistics | |

|

| Public Company Information | |

|

| Key Private Companies | |

|

| Government Vendors | |

|

| Instant Download - Available immediately upon purchase | |

|

| Download both PDF and Excel

|

|

|

| Download now: |

2026 U.S. Industry Statistics & Market Forecast - Electric Power Generation, Transmission and Distribution

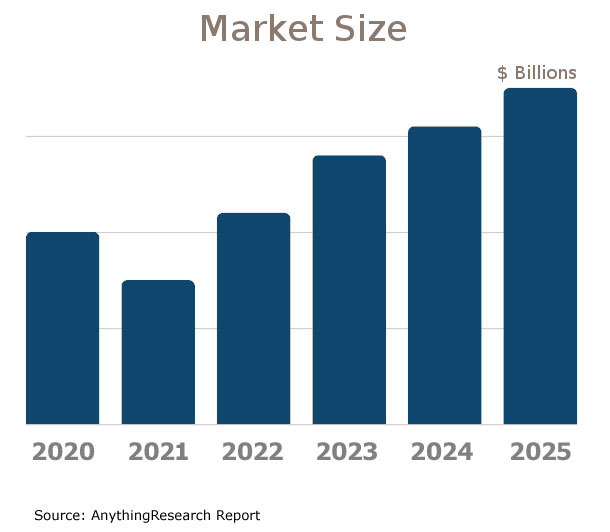

Market Size & Industry Statistics

The total U.S. industry market size for Electric Power Generation, Transmission and Distribution:

Industry statistics cover all companies in the United States, both public and private, ranging in size from small businesses to market leaders.

In addition to revenue, the industry market analysis shows information on employees, companies, and average firm size.

Investors, banks, and business executives use growth rates and industry trends to understand the market outlook and opportunity.

| Statistics | 2020 2021 2022 2023 2024 2025 | |

|---|---|---|

| Market Size (Total Sales/Revenue) |

Order at top of page | |

| Total Firms | ||

| Total Employees | ||

| Average Revenue Per Firm | ||

| Average Employees Per Firm | ||

| Average Revenue Per Employee | ||

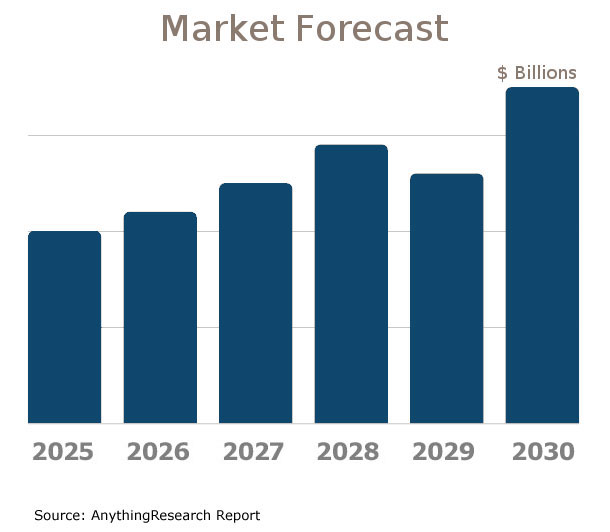

Market Forecast

Market forecasts show the long term industry outlook and future growth trends. The following extended five-year forecast projects both short-term and long-term trends.

| Forecast / Industry Outlook | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

|---|---|---|---|---|---|---|

| Market Forecast ($ millions) | ||||||

| Projected Industry Growth Rate (%) | ||||||

Industry Insights

Major trends affect the Electric Power Generation, Transmission and Distribution industry include:- Decarbonization and renewable energy integration

- Grid modernization and smart grid technologies

- Electrification of transportation

- Energy storage advancements

- Regulatory and policy changes

- Cybersecurity enhancement

- Climate change and resilience planning

- Distributed energy resource (DER) growth

- Consumer demand for transparency and control

- Increased focus on energy efficiency and demand response

- Digitalization and use of artificial intelligence (AI)

- Cross-sector electrification (heating, cooling, industrial processes)

Product & Services Breakdown

Research products and services in the Electric Power Generation, Transmission and Distribution industry generating sales. Note that products are broken into categories with different levels of classification.| Product Description | Number of Companies | Sales ($ millions) | Percent of Total Sales |

|---|---|---|---|

Industry Total |

|||

Transportation Of Bulk Natural Gas And Liquefied Natural Gas By Pipeline |

|||

Electricity - Power Marketing And Brokering |

|||

Natural Gas Distribution To Final Consumer |

|||

Natural Gas - Power Marketing And Brokering |

|||

Steam And/Or Air-Conditioning |

|||

Electric Power Transmission |

|||

Electricity - Generation |

|||

Electricity - Distribution |

|||

Other Products |

|||

U.S. Geographic Distribution: Revenue Statistics by State

Market Size by State ($ millions) indicates how the industry's competition is distributed throughout the country. State-level information can identify areas with higher and lower industry market share than average.

Income Statement (Average Financial Metrics)

Financial metrics provide a snapshot view of a benchmark "average" company. Key business metrics show revenue and operating costs. The data collected covers both public and private companies.| Industry Average | Percent of Sales (Industry Benchmark) |

|

|---|---|---|

| Total Revenue | Order at top of page |

|

| Operating Revenue | ||

| Cost of Goods Sold | ||

| Gross Profit | ||

Operating Expenses | ||

| Pension, profit sharing plans, stock, annuity | ||

| Repairs | ||

| Rent paid on business property | ||

| Charitable Contributions | ||

| Depletion | ||

| Domestic production activities deduction | ||

| Advertising | ||

| Compensation of officers | ||

| Salaries and wages | ||

| Employee benefit programs | ||

| Taxes and Licenses | ||

| Bad Debts | ||

| Depreciation | ||

| Amortization | ||

| Other Operating Expenses | ||

| Total Operating Expenses | ||

| Operating Income | ||

| Non-Operating Income | ||

| EBIT (Earnings Before Interest and Taxes) | ||

| Interest Expense | ||

| Earnings Before Taxes | ||

| Income Tax | ||

| Net Profit Net Income | ||

Financial Ratio Analysis

Financial ratio information can be used to benchmark how a Electric Power Generation, Transmission and Distribution company compares to its peers. Accounting statistics are calculated from the industry-average for income statements and balance sheets.| Profitability & Valuation Ratios | Industry Average |

|---|---|

| Company valuation can be measured based on the firm's own performance, as well as in comparison against its industry competitors. These metrics show how the average company in the Electric Power Generation, Transmission and Distribution industry is performing. | |

| Profit Margin Gross Profit Margin, Operating Profit Margin, and Net Profit Margin. Show company earnings relative to revenues. |

|

| Return on Equity (ROE) Return on Equity (ROE) is net income as a percentage of shareholders' equity. Shareholders' Equity is defined as the company's total assets minus total liabilities. ROE shows how much profits a company generates with the money shareholders invested (or with retained earnings). |

|

| Return on Assets (ROA) Return on Assets (ROA) is net income relative to total assets. The market research on Electric Power Generation, Transmission and Distribution measures how efficiently the company leverages its assets to generate profit. ROA is calculated as Net Income divided by Total Assets. |

|

| Liquidity Ratios | Industry Average |

|---|---|

| Bankers and suppliers use liquidity to determine creditworthiness and identify potential threats to a company's financial viability. | |

| Current Ratio Measures a firm's ability to pay its debts over the next 12 months. |

|

| Quick Ratio (Acid Test) Calculates liquid assets relative to liabilities, excluding inventories. |

|

| Efficiency Ratios - Key Performance Indicators | Industry Average |

|---|---|

| Measure how quickly products and services sell, and effectively collections policies are implemented. | |

| Receivables Turnover Ratio If this number is low in your business when compared to the industry average in the research report, it may mean your payment terms are too lenient or that you are not doing a good enough job on collections. |

|

| Average Collection Period Based on the Receivables Turnover, this estimates the collection period in days. Calculated as 365 divided by the Receivables Turnover |

|

| Inventory Turnover A low turnover rate may point to overstocking, obsolescence, or deficiencies in the product line or marketing effort. |

|

| Fixed-Asset Turnover Generally, higher is better, since it indicates the business has less money tied up in fixed assets for each dollar of sales revenue. |

|

Compensation & Salary Surveys for Employees

Compensation statistics provides an accurate assessment of industry-specific jobs and national salary averages. This information can be used to identify which positions are most common, and high, low, and average annual wages.| Title | Percent of Workforce | Bottom Quartile | Average (Median) Salary | Upper Quartile |

|---|---|---|---|---|

| Management Occupations | 8% | Order at top of page |

||

| Top Executives | 5% | |||

| Chief Executives | 0% | |||

| General and Operations Managers | 5% | |||

| General and Operations Managers | 3% | |||

| Business and Financial Operations Occupations | 9% | |||

| Business Operations Specialists | 7% | |||

| Logisticians and Project Management Specialists | 6% | |||

| Project Management Specialists | 5% | |||

| Architecture and Engineering Occupations | 10% | |||

| Engineers | 7% | |||

| Electrical and Electronics Engineers | 8% | |||

| Electrical Engineers | 8% | |||

| Nuclear Engineers | 10% | |||

| Nuclear Engineers | 10% | |||

| Life, Physical, and Social Science Occupations | 12% | |||

| Life, Physical, and Social Science Technicians | 10% | |||

| Nuclear Technicians | 9% | |||

| Nuclear Technicians | 9% | |||

| Protective Service Occupations | 11% | |||

| Other Protective Service Workers | 9% | |||

| Security Guards and Gambling Surveillance Officers | 9% | |||

| Security Guards | 9% | |||

| Sales and Related Occupations | 6% | |||

| Office and Administrative Support Occupations | 13% | |||

| Construction and Extraction Occupations | 27% | |||

| Construction Trades Workers | 23% | |||

| Electricians | 6% | |||

| Electricians | 6% | |||

| Solar Photovoltaic Installers | 15% | |||

| Solar Photovoltaic Installers | 15% | |||

| Installation, Maintenance, and Repair Occupations | 32% | |||

| Electrical and Electronic Equipment Mechanics, Installers, and Repairers | 6% | |||

| Miscellaneous Electrical and Electronic Equipment Mechanics, Installers, and Repairers | 6% | |||

| Electrical and Electronics Repairers, Powerhouse, Substation, and Relay | 6% | |||

| Other Installation, Maintenance, and Repair Occupations | 22% | |||

| Industrial Machinery Installation, Repair, and Maintenance Workers | 7% | |||

| Industrial Machinery Mechanics | 7% | |||

| Line Installers and Repairers | 15% | |||

| Electrical Power-Line Installers and Repairers | 15% | |||

| Wind Turbine Service Technicians | 41% | |||

| Wind Turbine Service Technicians | 41% | |||

| Production Occupations | 12% | |||

| Supervisors of Production Workers | 5% | |||

| First-Line Supervisors of Production and Operating Workers | 5% | |||

| First-Line Supervisors of Production and Operating Workers | 5% | |||

| Plant and System Operators | 9% | |||

| Power Plant Operators, Distributors, and Dispatchers | 9% | |||

| Nuclear Power Reactor Operators | 12% | |||

| Power Plant Operators | 6% | |||

Electric Power Generation, Transmission and Distribution Competitor Landscape & Key Companies [PREMIUM]

The most influential companies in the Electric Power Generation, Transmission and Distribution industry and adjacent industries either have large market share or are developing new business models and methods that could disrupt the status quo. We look at leading and emerging companies in the Electric Power Generation, Transmission and Distribution industry and adjacent sectors:| Market Leaders: Direct Competitors Companies with the largest market share, focused in this industry |

Market leaders: Diversified Competitors Largest companies that have diversified operations in this and other industries |

| Innovators: Direct Competitors Innovative, Emerging, and Disruptive Companies that may influence the future direction of the industry. |

Innovators: Diversified Competitors Innovators and Disruptors in adjacent industries that may also affect the Electric Power Generation, Transmission and Distribution industry. |

Latest Industry News

- Bunge Global (BG) Divests North America Dry Corn and Masa Milling Business - Bunge Global SA (NYSE:BG) is one of the 10 best organic food and farming stocks to buy now. On July 1, the company announced the sale of its North America dry corn and Corn masa milling business. The divestment came as the company strived to streamline operations ahead of its planned merger with Canadian grain (07/08/2025)

- Bunge sells North America corn milling unit - Bunge has completed the sale of its North America dry corn and corn masa milling business, the company announced yesterday (1 July 2025) as it continues to streamline operations ahead of its planned merger with Canadian grain handler Viterra. (07/04/2025)

- Bedford grower assesses new varieties to replace Extase - Matt Fuller is set to switch to two new milling wheat varieties this autumn to replace much of his Extase area if the Group 2 millers fulfil their promise (07/02/2025)

- Chattanooga-based Grain Craft adds 600 employees - Chattanooga-based Grain Craft, the largest independent wheat flour miller in the U.S., closed Tuesday on an expansive purchase of North American dry corn milling facilities, the company announced ... (07/01/2025)

- Grain futures surge amid Middle East unrest - Thunderstorms, soaring wheat futures and global supply shifts—how June weather and geopolitics are shaking up grain markets. (06/29/2025)

- Olam Agri partnership supports Nigerian soybean farmers - LAGOS, NIGERIA — Olam Agri has joined a strategic partnership with IDH, which brings together public and private stakeholders for sustainable and inclusive agriculture, and Arzikin Noma, a Nigerian agricultural development firm working in rural farming communities, to support soybean production in Nigeria’s Kwara State. (06/26/2025)

- Bühler Networking Days address sustainability, collaboration - The Networking Days 2025 was the fourth Bühler Group Networking Days event. The Swiss-based technology group has convened leaders from the industries it serves once every three years since 2016. Attendees at this year's event traveled from 90 countries and six continents. (06/26/2025)

- How Beds grower optimises second and third wheat yields - Variety choice is an important component of successful second or subsequent wheats and although Nabim Group 1 milling wheat Skyfall does have weaknesses, such as susceptibility to yellow rust, it ... (06/09/2025)

- Texas House OKs bill to boost power grid protection, strengthen ERCOT's emergency authority - The legislation, which now returns to the Senate for review, encourages large-scale users to develop backup power sources. (05/27/2025)

- Crack the whip to rescue discoms and energise reform - The time has come for the Modi Government to decisively untangle the sector from entrenched political interference, empower regulators, and open the door to private competition. Without bold, top-level reforms, (05/27/2025)