| Standard Report | Premium Report | |

|---|---|---|

| Current State of the Industry |  |

|

| Market Size (industry trends) | |

|

| Market Forecast (5-year projection) | |

|

| Products/Services Breakdown | |

|

| Revenue per State | |

|

| Financial Metrics | |

|

| Salary & Compensation Statistics | |

|

| Public Company Information | |

|

| Key Private Companies | |

|

| Government Vendors | |

|

| Instant Download - Available immediately upon purchase | |

|

| Download both PDF and Excel

|

|

|

| Download now: |

2026 U.S. Industry Statistics & Market Forecast - Credit Unions

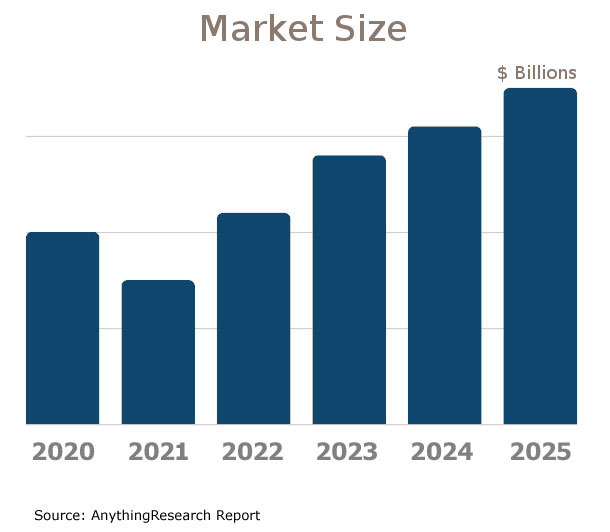

Market Size & Industry Statistics

The total U.S. industry market size for Credit Unions:

Industry statistics cover all companies in the United States, both public and private, ranging in size from small businesses to market leaders.

In addition to revenue, the industry market analysis shows information on employees, companies, and average firm size.

Investors, banks, and business executives use growth rates and industry trends to understand the market outlook and opportunity.

| Statistics | 2020 2021 2022 2023 2024 2025 | |

|---|---|---|

| Market Size (Total Sales/Revenue) |

Order at top of page | |

| Total Firms | ||

| Total Employees | ||

| Average Revenue Per Firm | ||

| Average Employees Per Firm | ||

| Average Revenue Per Employee | ||

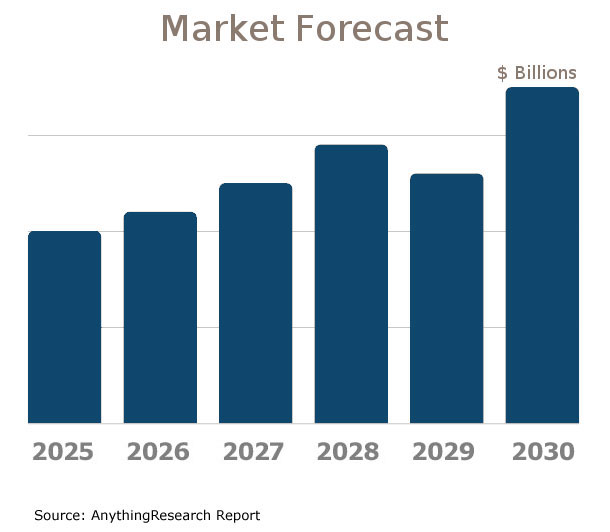

Market Forecast

Market forecasts show the long term industry outlook and future growth trends. The following extended five-year forecast projects both short-term and long-term trends.

| Forecast / Industry Outlook | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

|---|---|---|---|---|---|---|

| Market Forecast ($ millions) | ||||||

| Projected Industry Growth Rate (%) | ||||||

Industry Insights

Major trends affect the Credit Unions industry include:- Increased digitalization and mobile banking adoption

- Rising cybersecurity threats and investment in security technology

- Regulatory changes and compliance pressures

- Shift towards more personalized customer service experiences

- Expansion of services to compete with traditional banks and fintech

- Growing emphasis on community and social responsibility

- Interest rate fluctuations impacting profitability

- Adoption of AI and machine learning for operational efficiency

- Demographic shifts, including aging membership bases

- Integration of sustainable and green financing options

- Challenges in maintaining the credit union tax-exempt status

- Increased collaboration and partnerships within the financial industry

- Pressure on net interest margins leading to innovation in fee-based services

- Enhancement of remote services post-pandemic recovery efforts

- Focus on financial literacy programs to engage younger members

- Consolidation and mergers to achieve economies of scale and expand geographic reach

Product & Services Breakdown

Research products and services in the Credit Unions industry generating sales. Note that products are broken into categories with different levels of classification.| Product Description | Number of Companies | Sales ($ millions) | Percent of Total Sales |

|---|---|---|---|

Industry Total |

|||

Loan Services - Income |

|||

Loans To Financial Businesses |

|||

Loans To Non-Financial Businesses |

|||

Residential Mortgage Loans |

|||

Home Equity Loans |

|||

Vehicle Loans, Consumer |

|||

All Other Secured Or Guaranteed Loans To Consumers |

|||

Unsecured Loans To Consumers |

|||

Credit Card Services - Income |

|||

Credit Card Services For Cardholders, Business And Government |

|||

Credit Card Services For Cardholders, Consumer |

|||

Credit Card Services For Merchants |

|||

Credit Card Association Products |

|||

Factoring Services - Fees |

|||

Other Credit Financing Services - Income |

|||

Financing Related To Securities |

|||

Trading Debt Instruments On Own Account - Net Gains (Losses) |

|||

Trading Other Securities And Commodity Contracts On Own Account - Net Gains (Losses) |

|||

Deposit Account Service Packages, Except Business |

|||

Separately-Priced Deposit Account Services, Except Business |

|||

Cash Handling And Management Services For Business |

|||

Document Payment Services |

|||

Automated Clearinghouse (Ach) Services - Fees |

|||

Financial Planning And Investment Management Services |

|||

Other Products Supporting Financial Services - Fees |

|||

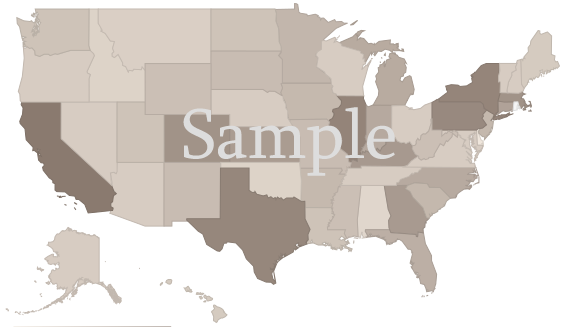

U.S. Geographic Distribution: Revenue Statistics by State

Market Size by State ($ millions) indicates how the industry's competition is distributed throughout the country. State-level information can identify areas with higher and lower industry market share than average.

Income Statement (Average Financial Metrics)

Financial metrics provide a snapshot view of a benchmark "average" company. Key business metrics show revenue and operating costs. The data collected covers both public and private companies.| Industry Average | Percent of Sales (Industry Benchmark) |

|

|---|---|---|

| Total Revenue | Order at top of page |

|

| Operating Revenue | ||

| Cost of Goods Sold | ||

| Gross Profit | ||

Operating Expenses | ||

| Pension, profit sharing plans, stock, annuity | ||

| Repairs | ||

| Rent paid on business property | ||

| Charitable Contributions | ||

| Depletion | ||

| Domestic production activities deduction | ||

| Advertising | ||

| Compensation of officers | ||

| Salaries and wages | ||

| Employee benefit programs | ||

| Taxes and Licenses | ||

| Bad Debts | ||

| Depreciation | ||

| Amortization | ||

| Other Operating Expenses | ||

| Total Operating Expenses | ||

| Operating Income | ||

| Non-Operating Income | ||

| EBIT (Earnings Before Interest and Taxes) | ||

| Interest Expense | ||

| Earnings Before Taxes | ||

| Income Tax | ||

| Net Profit Net Income | ||

Financial Ratio Analysis

Financial ratio information can be used to benchmark how a Credit Unions company compares to its peers. Accounting statistics are calculated from the industry-average for income statements and balance sheets.| Profitability & Valuation Ratios | Industry Average |

|---|---|

| Company valuation can be measured based on the firm's own performance, as well as in comparison against its industry competitors. These metrics show how the average company in the Credit Unions industry is performing. | |

| Profit Margin Gross Profit Margin, Operating Profit Margin, and Net Profit Margin. Show company earnings relative to revenues. |

|

| Return on Equity (ROE) Return on Equity (ROE) is net income as a percentage of shareholders' equity. Shareholders' Equity is defined as the company's total assets minus total liabilities. ROE shows how much profits a company generates with the money shareholders invested (or with retained earnings). |

|

| Return on Assets (ROA) Return on Assets (ROA) is net income relative to total assets. The market research on Credit Unions measures how efficiently the company leverages its assets to generate profit. ROA is calculated as Net Income divided by Total Assets. |

|

| Liquidity Ratios | Industry Average |

|---|---|

| Bankers and suppliers use liquidity to determine creditworthiness and identify potential threats to a company's financial viability. | |

| Current Ratio Measures a firm's ability to pay its debts over the next 12 months. |

|

| Quick Ratio (Acid Test) Calculates liquid assets relative to liabilities, excluding inventories. |

|

| Efficiency Ratios - Key Performance Indicators | Industry Average |

|---|---|

| Measure how quickly products and services sell, and effectively collections policies are implemented. | |

| Receivables Turnover Ratio If this number is low in your business when compared to the industry average in the research report, it may mean your payment terms are too lenient or that you are not doing a good enough job on collections. |

|

| Average Collection Period Based on the Receivables Turnover, this estimates the collection period in days. Calculated as 365 divided by the Receivables Turnover |

|

| Inventory Turnover A low turnover rate may point to overstocking, obsolescence, or deficiencies in the product line or marketing effort. |

|

| Fixed-Asset Turnover Generally, higher is better, since it indicates the business has less money tied up in fixed assets for each dollar of sales revenue. |

|

Compensation & Salary Surveys for Employees

Compensation statistics provides an accurate assessment of industry-specific jobs and national salary averages. This information can be used to identify which positions are most common, and high, low, and average annual wages.| Title | Percent of Workforce | Bottom Quartile | Average (Median) Salary | Upper Quartile |

|---|---|---|---|---|

| Management Occupations | 11% | Order at top of page |

||

| Chief Executives | 0% | |||

| General and Operations Managers | 3% | |||

| Operations Specialties Managers | 6% | |||

| Business and Financial Operations Occupations | 26% | |||

| Business Operations Specialists | 6% | |||

| Financial Specialists | 20% | |||

| Credit Counselors and Loan Officers | 11% | |||

| Loan Officers | 11% | |||

| Computer and Mathematical Occupations | 7% | |||

| Computer Occupations | 6% | |||

| Sales and Related Occupations | 13% | |||

| Sales Representatives, Services | 10% | |||

| Securities, Commodities, and Financial Services Sales Agents | 10% | |||

| Securities, Commodities, and Financial Services Sales Agents | 10% | |||

| Office and Administrative Support Occupations | 42% | |||

| Financial Clerks | 18% | |||

| Tellers | 13% | |||

| Tellers | 13% | |||

| Information and Record Clerks | 17% | |||

| Customer Service Representatives | 7% | |||

| Customer Service Representatives | 7% | |||

| Loan Interviewers and Clerks | 7% | |||

| Loan Interviewers and Clerks | 7% | |||

Credit Unions Competitor Landscape & Key Companies [PREMIUM]

The most influential companies in the Credit Unions industry and adjacent industries either have large market share or are developing new business models and methods that could disrupt the status quo. We look at leading and emerging companies in the Credit Unions industry and adjacent sectors:| Market Leaders: Direct Competitors Companies with the largest market share, focused in this industry |

Market leaders: Diversified Competitors Largest companies that have diversified operations in this and other industries |

| Innovators: Direct Competitors Innovative, Emerging, and Disruptive Companies that may influence the future direction of the industry. |

Innovators: Diversified Competitors Innovators and Disruptors in adjacent industries that may also affect the Credit Unions industry. |

Latest Industry News

- MIDFLORIDA Credit Union Amphitheatre adds 'Backyard' for concertgoers - The newest premium area at the MIDFLORIDA Credit Union Amphitheatre was designed to show off what a Florida summer has to offer. (07/08/2025)

- First West Credit Union releases inaugural Impact Report demonstrating community leadership and social impact - LANGLEY, B.C., July 08, 2025 (GLOBE NEWSWIRE) -- First West Credit Union has released its first-ever Impact Report, showcasing how the member-owned cooperative is balancing financial performance with meaningful social, environmental and community impact across British Columbia. (07/08/2025)

- Veridian Credit Union plans new Eden Prairie branch - Veridian Credit Union will open its second Twin Cities location with a branch that's in a much busier area than the spot it acquired when it entered the market in 2023. (07/08/2025)

- Bow Valley Credit Union in Canada turns on Bitcoin purchases for Albertans - BVCU’s Bitcoin Gateway, with Balance Custody and Bull Bitcoin API, simplifies buying bitcoin. “Facilitates institutional adoption,” says Francis Pouliot. (07/08/2025)

- LGE Community Credit Union - Dedicated to the health and advancement of members' financial lives and its communities. (07/08/2025)

- Firelands Federal Credit Union Selects Mahalo Banking to Deepen Member Engagement - Firelands FCU selects Mahalo Banking to deliver a modern, secure digital experience with flexible tools and seamless third-party integrations. (07/08/2025)

- Merger creates new $125M credit union with expanded metro network - LEE’S SUMMIT, Mo. (KCTV) - A pair of metro area credit unions have merged to amplify the Missouri Central Credit Union, an expanded network worth $125 million. The Missouri Central Credit Union announced on Monday, July 7, that it has finalized a merger agreement with Central Communications Credit Union, effective May 31, 2025. (07/08/2025)

- Let's Talk Business: Grand openings set for Jersey Mike's and Bellco Credit Union - Grand openings are set for a new Jersey Mike's sub shop in Pueblo West and a new Bellco Credit Union branch in Pueblo. (07/07/2025)

- TDECU delays rebrand as it closes Space City Credit Union merger, terminates bank acquisition - After quietly closing a merger and terminating an acquisition, Houston's largest credit union has delayed another change. (07/03/2025)

- Navy Federal Credit Union no longer has to refund $80 million in overdraft fees. Here's why. - The Consumer Financial Protection Bureau terminated an order requiring NFCU to reimburse $80 million to customers. (07/02/2025)