| Standard Report | Premium Report | |

|---|---|---|

| Current State of the Industry |  |

|

| Market Size (industry trends) | |

|

| Market Forecast (5-year projection) | |

|

| Products/Services Breakdown | |

|

| Revenue per State | |

|

| Financial Metrics | |

|

| Salary & Compensation Statistics | |

|

| Public Company Information | |

|

| Key Private Companies | |

|

| Government Vendors | |

|

| Instant Download - Available immediately upon purchase | |

|

| Download both PDF and Excel

|

|

|

| Download now: |

2026 U.S. Industry Statistics & Market Forecast - Consumer Lending

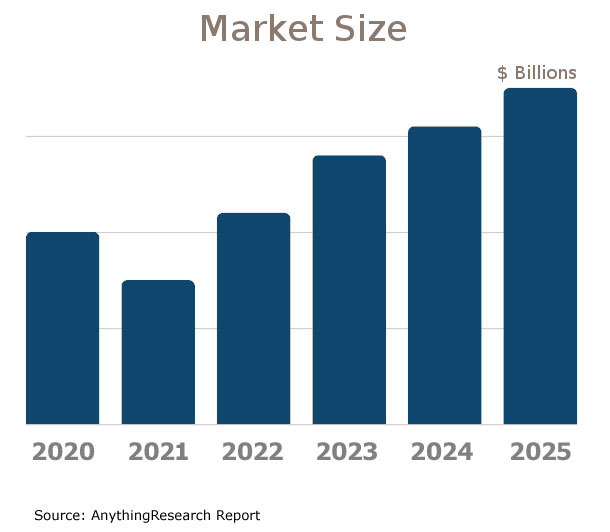

Market Size & Industry Statistics

The total U.S. industry market size for Consumer Lending:

Industry statistics cover all companies in the United States, both public and private, ranging in size from small businesses to market leaders.

In addition to revenue, the industry market analysis shows information on employees, companies, and average firm size.

Investors, banks, and business executives use growth rates and industry trends to understand the market outlook and opportunity.

| Statistics | 2020 2021 2022 2023 2024 2025 | |

|---|---|---|

| Market Size (Total Sales/Revenue) |

Order at top of page | |

| Total Firms | ||

| Total Employees | ||

| Average Revenue Per Firm | ||

| Average Employees Per Firm | ||

| Average Revenue Per Employee | ||

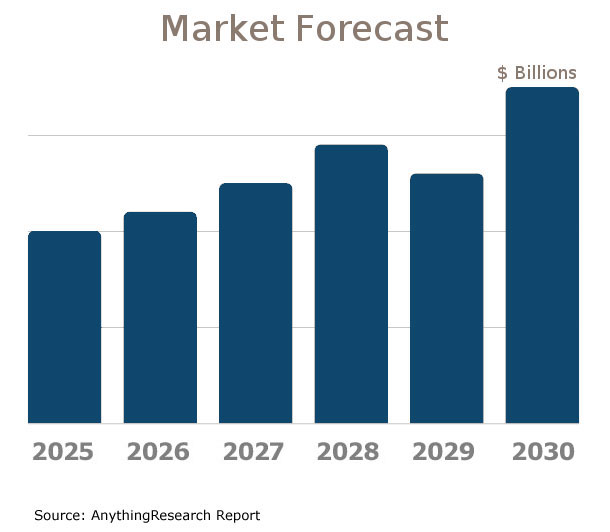

Market Forecast

Market forecasts show the long term industry outlook and future growth trends. The following extended five-year forecast projects both short-term and long-term trends.

| Forecast / Industry Outlook | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

|---|---|---|---|---|---|---|

| Market Forecast ($ millions) | ||||||

| Projected Industry Growth Rate (%) | ||||||

Industry Insights

Major trends affect the Consumer Lending industry include:- Digitization and online lending growth

- Increased regulatory scrutiny

- Consumer demand for transparency and simpler products

- Rising interest rates

- Growth in alternative lending platforms

- Greater focus on sustainable and ethical lending practices

- Use of big data and analytics for personalized offerings

- Integration of AI and machine learning for credit assessments

- Impact of economic slowdowns on consumer credit quality

- Shift towards flexible payment solutions and buy now, pay later options

- Expansion of financial services by non-traditional institutions

- Increased importance of cybersecurity and data protection

Product & Services Breakdown

Research products and services in the Consumer Lending industry generating sales. Note that products are broken into categories with different levels of classification.| Product Description | Number of Companies | Sales ($ millions) | Percent of Total Sales |

|---|---|---|---|

Industry Total |

|||

Loan Services - Income |

|||

Loans To Financial Businesses |

|||

Loans To Non-Financial Businesses |

|||

Residential Mortgage Loans |

|||

Vehicle Loans, Consumer |

|||

All Other Secured Or Guaranteed Loans To Consumers |

|||

Unsecured Loans To Consumers |

|||

Leasing Services - Income |

|||

Operating Leases - Other |

|||

Installment Credit Services - Income |

|||

Sales Financing, Business |

|||

Sales Financing, Consumer |

|||

Other Credit Financing Services - Income |

|||

Other Products Supporting Financial Services - Fees |

|||

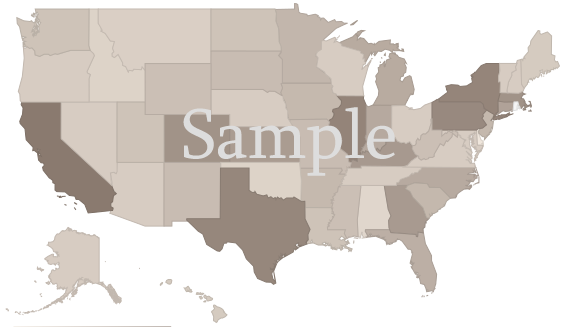

U.S. Geographic Distribution: Revenue Statistics by State

Market Size by State ($ millions) indicates how the industry's competition is distributed throughout the country. State-level information can identify areas with higher and lower industry market share than average.

Income Statement (Average Financial Metrics)

Financial metrics provide a snapshot view of a benchmark "average" company. Key business metrics show revenue and operating costs. The data collected covers both public and private companies.| Industry Average | Percent of Sales (Industry Benchmark) |

|

|---|---|---|

| Total Revenue | Order at top of page |

|

| Operating Revenue | ||

| Cost of Goods Sold | ||

| Gross Profit | ||

Operating Expenses | ||

| Pension, profit sharing plans, stock, annuity | ||

| Repairs | ||

| Rent paid on business property | ||

| Charitable Contributions | ||

| Depletion | ||

| Domestic production activities deduction | ||

| Advertising | ||

| Compensation of officers | ||

| Salaries and wages | ||

| Employee benefit programs | ||

| Taxes and Licenses | ||

| Bad Debts | ||

| Depreciation | ||

| Amortization | ||

| Other Operating Expenses | ||

| Total Operating Expenses | ||

| Operating Income | ||

| Non-Operating Income | ||

| EBIT (Earnings Before Interest and Taxes) | ||

| Interest Expense | ||

| Earnings Before Taxes | ||

| Income Tax | ||

| Net Profit Net Income | ||

Financial Ratio Analysis

Financial ratio information can be used to benchmark how a Consumer Lending company compares to its peers. Accounting statistics are calculated from the industry-average for income statements and balance sheets.| Profitability & Valuation Ratios | Industry Average |

|---|---|

| Company valuation can be measured based on the firm's own performance, as well as in comparison against its industry competitors. These metrics show how the average company in the Consumer Lending industry is performing. | |

| Profit Margin Gross Profit Margin, Operating Profit Margin, and Net Profit Margin. Show company earnings relative to revenues. |

|

| Return on Equity (ROE) Return on Equity (ROE) is net income as a percentage of shareholders' equity. Shareholders' Equity is defined as the company's total assets minus total liabilities. ROE shows how much profits a company generates with the money shareholders invested (or with retained earnings). |

|

| Return on Assets (ROA) Return on Assets (ROA) is net income relative to total assets. The market research on Consumer Lending measures how efficiently the company leverages its assets to generate profit. ROA is calculated as Net Income divided by Total Assets. |

|

| Liquidity Ratios | Industry Average |

|---|---|

| Bankers and suppliers use liquidity to determine creditworthiness and identify potential threats to a company's financial viability. | |

| Current Ratio Measures a firm's ability to pay its debts over the next 12 months. |

|

| Quick Ratio (Acid Test) Calculates liquid assets relative to liabilities, excluding inventories. |

|

| Efficiency Ratios - Key Performance Indicators | Industry Average |

|---|---|

| Measure how quickly products and services sell, and effectively collections policies are implemented. | |

| Receivables Turnover Ratio If this number is low in your business when compared to the industry average in the research report, it may mean your payment terms are too lenient or that you are not doing a good enough job on collections. |

|

| Average Collection Period Based on the Receivables Turnover, this estimates the collection period in days. Calculated as 365 divided by the Receivables Turnover |

|

| Inventory Turnover A low turnover rate may point to overstocking, obsolescence, or deficiencies in the product line or marketing effort. |

|

| Fixed-Asset Turnover Generally, higher is better, since it indicates the business has less money tied up in fixed assets for each dollar of sales revenue. |

|

Compensation & Salary Surveys for Employees

Compensation statistics provides an accurate assessment of industry-specific jobs and national salary averages. This information can be used to identify which positions are most common, and high, low, and average annual wages.| Title | Percent of Workforce | Bottom Quartile | Average (Median) Salary | Upper Quartile |

|---|---|---|---|---|

| Management Occupations | 12% | Order at top of page |

||

| Chief Executives | 0% | |||

| General and Operations Managers | 5% | |||

| Operations Specialties Managers | 6% | |||

| Business and Financial Operations Occupations | 35% | |||

| Business Operations Specialists | 5% | |||

| Financial Specialists | 30% | |||

| Credit Counselors and Loan Officers | 23% | |||

| Loan Officers | 23% | |||

| Sales and Related Occupations | 11% | |||

| Office and Administrative Support Occupations | 36% | |||

| Information and Record Clerks | 24% | |||

| Customer Service Representatives | 6% | |||

| Customer Service Representatives | 6% | |||

| Loan Interviewers and Clerks | 18% | |||

| Loan Interviewers and Clerks | 18% | |||

Consumer Lending Competitor Landscape & Key Companies [PREMIUM]

The most influential companies in the Consumer Lending industry and adjacent industries either have large market share or are developing new business models and methods that could disrupt the status quo. We look at leading and emerging companies in the Consumer Lending industry and adjacent sectors:| Market Leaders: Direct Competitors Companies with the largest market share, focused in this industry |

Market leaders: Diversified Competitors Largest companies that have diversified operations in this and other industries |

| Innovators: Direct Competitors Innovative, Emerging, and Disruptive Companies that may influence the future direction of the industry. |

Innovators: Diversified Competitors Innovators and Disruptors in adjacent industries that may also affect the Consumer Lending industry. |

Latest Industry News

- FHA seeks input on buy now, pay later lending - The FHA has opened a request for information on BNPL lending as it seeks to understand implications for housing affordability and stability. (07/07/2025)

- UK lenders report surprise rise in mortgages in May, consumer lending cools - The number of mortgages approved by British lenders for house purchases unexpectedly jumped in May, according to Bank of England data that suggested the housing market recovered quickly from the end of a tax break for homebuyers in April. (07/06/2025)

- Consumer boycotts continue: 31% are participating. See where and why - As consumer boycotts, which started earlier this year continue and expand, a new study is showing that nearly a third of consumers surveyed have participated in such an action. (07/03/2025)

- Senate passes budget bill slashing social safety net and consumer protections - Senate passes reconciliation bill 51-50, with Vice President Vance casting tie-breaking vote, threatening healthcare, consumer protections, and student loa (07/02/2025)

- Consumer group condemns withdrawal of Navy Federal penalty - Consumer Federation of America slams CFPB’s reversal of a $95 million consent order against Navy Federal Credit Union for illegal overdraft fees. A (07/02/2025)

- Don't let them take it: banks are reluctant to lower consumer loan rates - Banks are reluctant to lower consumer loan rates — only six of the top 15 players did so in June, Izvestia found. On average, interest rates on loans fell by less than 1 percentage point, to 34%. This is despite the fact that at the beginning of last month, (07/02/2025)

- Consumer panel bars loan recovery from widow, penalises firm for insurance lapse - TIRUNELVELI: Tirunelveli District Consumer Disputes Redressal Commission on Thursday ordered a finance company not to collect a loan of Rs 15 lakh borrowed by t (06/28/2025)

- Buy Now, Pay Later loans will soon affect some credit scores - Typically, when using Buy Now, Pay Later loans, consumers pay for a given purchase in four installments over six weeks, in a model more similar to layaway than to a traditional credit card. The loans are marketed as zero-interest, and most require no credit check or only a soft credit check. (06/26/2025)

- How to escape the payday loan debt cycle, according to experts - Experts recommend taking certain steps now if you're trying to escape a payday loan debt cycle. Here's how to do it. (05/26/2025)

- Why are more shoppers struggling to repay ‘buy now, pay later’ loans? - NEW YORK — More Klarna customers are having trouble repaying their “buy now, pay later” loans, the short-term lender said this week. The disclosure corresponded with reports by lending platforms Bankrate and LendingTree, which cited an increasing share of all “buy now, pay later” users saying they had fallen behind on payments. (05/23/2025)