| Standard Report | Premium Report | |

|---|---|---|

| Current State of the Industry |  |

|

| Market Size (industry trends) | |

|

| Market Forecast (5-year projection) | |

|

| Products/Services Breakdown | |

|

| Revenue per State | |

|

| Financial Metrics | |

|

| Salary & Compensation Statistics | |

|

| Public Company Information | |

|

| Key Private Companies | |

|

| Government Vendors | |

|

| Instant Download - Available immediately upon purchase | |

|

| Download both PDF and Excel

|

|

|

| Download now: |

2026 U.S. Industry Statistics & Market Forecast - Credit Intermediation

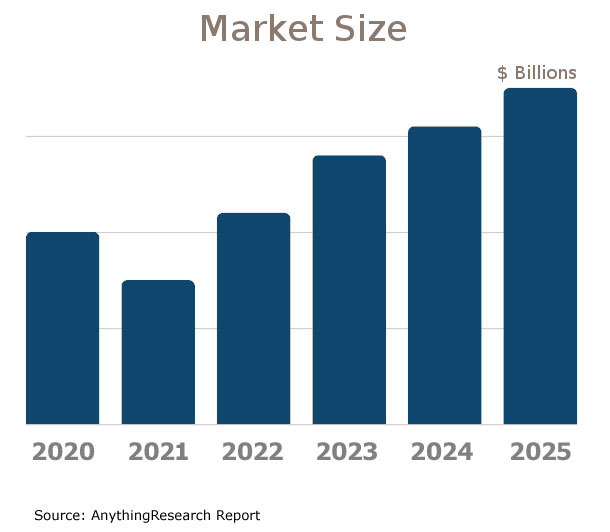

Market Size & Industry Statistics

The total U.S. industry market size for Credit Intermediation:

Industry statistics cover all companies in the United States, both public and private, ranging in size from small businesses to market leaders.

In addition to revenue, the industry market analysis shows information on employees, companies, and average firm size.

Investors, banks, and business executives use growth rates and industry trends to understand the market outlook and opportunity.

| Statistics | 2020 2021 2022 2023 2024 2025 | |

|---|---|---|

| Market Size (Total Sales/Revenue) |

Order at top of page | |

| Total Firms | ||

| Total Employees | ||

| Average Revenue Per Firm | ||

| Average Employees Per Firm | ||

| Average Revenue Per Employee | ||

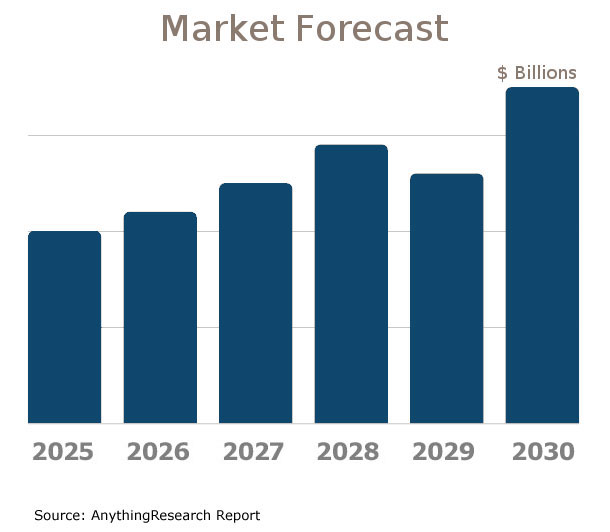

Market Forecast

Market forecasts show the long term industry outlook and future growth trends. The following extended five-year forecast projects both short-term and long-term trends.

| Forecast / Industry Outlook | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

|---|---|---|---|---|---|---|

| Market Forecast ($ millions) | ||||||

| Projected Industry Growth Rate (%) | ||||||

Industry Insights

Major trends affect the Credit Intermediation industry include:- Increasing regulatory scrutiny and compliance costs

- Rising adoption of fintech and digital-only banking platforms

- Growth in use of artificial intelligence and machine learning for risk assessment

- Higher demand for transparency and enhanced customer service

- Integration of blockchain technology for secure and efficient transactions

- Shift towards sustainable and socially responsible lending

- Expansion of services to underserved markets through mobile and online banking

- Increased cybersecurity threats and need for robust protective measures

- Impact of economic fluctuations on loan demand and credit quality

- Growing importance of data analytics in customer acquisition and retention

Product & Services Breakdown

Research products and services in the Credit Intermediation industry generating sales. Note that products are broken into categories with different levels of classification.| Product Description | Number of Companies | Sales ($ millions) | Percent of Total Sales |

|---|---|---|---|

Industry Total |

|||

Loan Services - Income |

|||

Loans To Financial Businesses |

|||

Loans To Non-Financial Businesses |

|||

Residential Mortgage Loans |

|||

Vehicle Loans, Consumer |

|||

All Other Secured Or Guaranteed Loans To Consumers |

|||

Unsecured Loans To Consumers |

|||

Credit Card Services - Income |

|||

Credit Card Services For Cardholders, Business And Government |

|||

Credit Card Services For Cardholders, Consumer |

|||

Credit Card Services For Merchants |

|||

Credit Card Association Products |

|||

Other Credit Financing Services - Income |

|||

Brokering And Dealing Services For Debt Instruments |

|||

Trading Debt Instruments On Own Account - Net Gains (Losses) |

|||

Deposit Account Service Packages, Except Business |

|||

Separately-Priced Deposit Account Services, Except Business |

|||

Cash Handling And Management Services For Business |

|||

Document Payment Services |

|||

Automated Clearinghouse (Ach) Services - Fees |

|||

Other Products Supporting Financial Services - Fees |

|||

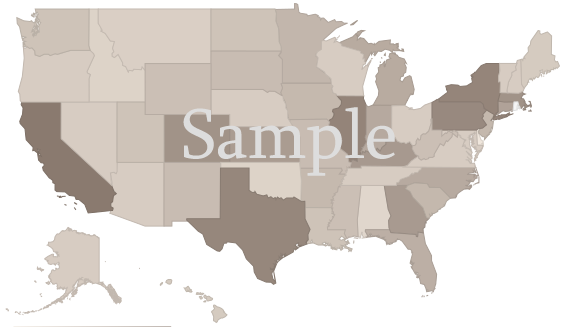

U.S. Geographic Distribution: Revenue Statistics by State

Market Size by State ($ millions) indicates how the industry's competition is distributed throughout the country. State-level information can identify areas with higher and lower industry market share than average.

Income Statement (Average Financial Metrics)

Financial metrics provide a snapshot view of a benchmark "average" company. Key business metrics show revenue and operating costs. The data collected covers both public and private companies.| Industry Average | Percent of Sales (Industry Benchmark) |

|

|---|---|---|

| Total Revenue | Order at top of page |

|

| Operating Revenue | ||

| Cost of Goods Sold | ||

| Gross Profit | ||

Operating Expenses | ||

| Pension, profit sharing plans, stock, annuity | ||

| Repairs | ||

| Rent paid on business property | ||

| Charitable Contributions | ||

| Depletion | ||

| Domestic production activities deduction | ||

| Advertising | ||

| Compensation of officers | ||

| Salaries and wages | ||

| Employee benefit programs | ||

| Taxes and Licenses | ||

| Bad Debts | ||

| Depreciation | ||

| Amortization | ||

| Other Operating Expenses | ||

| Total Operating Expenses | ||

| Operating Income | ||

| Non-Operating Income | ||

| EBIT (Earnings Before Interest and Taxes) | ||

| Interest Expense | ||

| Earnings Before Taxes | ||

| Income Tax | ||

| Net Profit Net Income | ||

Financial Ratio Analysis

Financial ratio information can be used to benchmark how a Credit Intermediation company compares to its peers. Accounting statistics are calculated from the industry-average for income statements and balance sheets.| Profitability & Valuation Ratios | Industry Average |

|---|---|

| Company valuation can be measured based on the firm's own performance, as well as in comparison against its industry competitors. These metrics show how the average company in the Credit Intermediation industry is performing. | |

| Profit Margin Gross Profit Margin, Operating Profit Margin, and Net Profit Margin. Show company earnings relative to revenues. |

|

| Return on Equity (ROE) Return on Equity (ROE) is net income as a percentage of shareholders' equity. Shareholders' Equity is defined as the company's total assets minus total liabilities. ROE shows how much profits a company generates with the money shareholders invested (or with retained earnings). |

|

| Return on Assets (ROA) Return on Assets (ROA) is net income relative to total assets. The market research on Credit Intermediation measures how efficiently the company leverages its assets to generate profit. ROA is calculated as Net Income divided by Total Assets. |

|

| Liquidity Ratios | Industry Average |

|---|---|

| Bankers and suppliers use liquidity to determine creditworthiness and identify potential threats to a company's financial viability. | |

| Current Ratio Measures a firm's ability to pay its debts over the next 12 months. |

|

| Quick Ratio (Acid Test) Calculates liquid assets relative to liabilities, excluding inventories. |

|

| Efficiency Ratios - Key Performance Indicators | Industry Average |

|---|---|

| Measure how quickly products and services sell, and effectively collections policies are implemented. | |

| Receivables Turnover Ratio If this number is low in your business when compared to the industry average in the research report, it may mean your payment terms are too lenient or that you are not doing a good enough job on collections. |

|

| Average Collection Period Based on the Receivables Turnover, this estimates the collection period in days. Calculated as 365 divided by the Receivables Turnover |

|

| Inventory Turnover A low turnover rate may point to overstocking, obsolescence, or deficiencies in the product line or marketing effort. |

|

| Fixed-Asset Turnover Generally, higher is better, since it indicates the business has less money tied up in fixed assets for each dollar of sales revenue. |

|

Compensation & Salary Surveys for Employees

Compensation statistics provides an accurate assessment of industry-specific jobs and national salary averages. This information can be used to identify which positions are most common, and high, low, and average annual wages.| Title | Percent of Workforce | Bottom Quartile | Average (Median) Salary | Upper Quartile |

|---|---|---|---|---|

| Management Occupations | 11% | Order at top of page |

||

| Chief Executives | 0% | |||

| General and Operations Managers | 3% | |||

| Operations Specialties Managers | 6% | |||

| Business and Financial Operations Occupations | 26% | |||

| Business Operations Specialists | 6% | |||

| Financial Specialists | 20% | |||

| Credit Counselors and Loan Officers | 11% | |||

| Loan Officers | 11% | |||

| Computer and Mathematical Occupations | 7% | |||

| Computer Occupations | 6% | |||

| Sales and Related Occupations | 13% | |||

| Sales Representatives, Services | 10% | |||

| Securities, Commodities, and Financial Services Sales Agents | 10% | |||

| Securities, Commodities, and Financial Services Sales Agents | 10% | |||

| Office and Administrative Support Occupations | 42% | |||

| Financial Clerks | 18% | |||

| Tellers | 13% | |||

| Tellers | 13% | |||

| Information and Record Clerks | 17% | |||

| Customer Service Representatives | 7% | |||

| Customer Service Representatives | 7% | |||

| Loan Interviewers and Clerks | 7% | |||

| Loan Interviewers and Clerks | 7% | |||

Credit Intermediation Competitor Landscape & Key Companies [PREMIUM]

The most influential companies in the Credit Intermediation industry and adjacent industries either have large market share or are developing new business models and methods that could disrupt the status quo. We look at leading and emerging companies in the Credit Intermediation industry and adjacent sectors:| Market Leaders: Direct Competitors Companies with the largest market share, focused in this industry |

Market leaders: Diversified Competitors Largest companies that have diversified operations in this and other industries |

| Innovators: Direct Competitors Innovative, Emerging, and Disruptive Companies that may influence the future direction of the industry. |

Innovators: Diversified Competitors Innovators and Disruptors in adjacent industries that may also affect the Credit Intermediation industry. |

Latest Industry News

- Credit & Risk in 2025: Managing Changing Credit Conditions through Experience, Discipline and Innovation - As uncertainty roils the economy, two chief risk officers reveal how they’re managing volatility, tightening standards and finding opportunity in a bifurcated lending landscape. (07/10/2025)

- The Week Ahead - Economists widely expect the central bank to cut the overnight policy rate (OPR) by 25 basis points (bps) to 2.75%. A recent Bloomberg survey found that eight out of 15 economists predict a rate cut, while a significant minority of seven expect the OPR to remain unchanged at 3%. (07/06/2025)

- Non-bank financial intermediation: Canada’s submission to the 2024 global monitoring report - We share insights about non-bank financial intermediation in Canada in 2023. These data were collected as part of the Bank of Canada’s contribution to the Financial Stability Board’s Global Monitoring Report on Non-Bank Financial Intermediation. (07/04/2025)

- Lending confidence rebounds: What’s behind the rise in South Africa's credit activity? - High interest rates initially boosted bank profits, but rising bad debt and credit impairments later weighed on earnings. As inflation fell and rates were cut, loan growth rebounded from 3.2% in ... (07/04/2025)

- Stability is the SLR proposal's goal — but it's no guarantee - Regulators hope changes to the supplementary leverage ratio will improve Treasury market function, but whether that happens depends in large part on how banks react and adapt. (07/01/2025)

- Pentagon intelligence agency pauses events, activities related to MLK Day, Black History Month - ABC News - Pentagon intelligence agency pauses events, activities related to MLK Day, Black History Month The pause comes after Trump targeted DEI initiatives in executive orders. (06/29/2025)

- The Corporate Profit Explosion Stalls In Q1 2025, On The Eve Of The New Tariffs - The explosion of corporate profits during the high-inflation years stalled in Q1, according to data from the Bureau of Economic Analysis today. (06/27/2025)

- Naira slides, but Nigeria’s bank assets jump 40% to N170 trillion in 2024 — SOE Report - Nigeria's banking sector posted significant growth in 2024, with total assets surging to N170.02 trillion, marking a 39.6% year-on-year increase (06/26/2025)

- Missing a rental payment or service fee will soon hit your credit score in the UAE - Gulf News - Dubai: Residents in the UAE will soon have payments related to their properties included in their credit score – whether that’s a rental payment or, in the case of property owners, their ... (06/11/2025)

- May Global Regulatory Brief: Trading and markets - Regulatory authorities continue to advance initiatives to improve the efficiency and sophistication of global securities markets. (05/28/2025)